22 June 2026

SUMMARY

➤ In a definitive break from forward guidance approach, newly minted Fed Chair Kevin Warsh led a divided Federal Reserve to maintain the target range at 3.50%–3.75%, with the Committee’s hawkish pivot in the median dot plot to 3.8% projecting tightening bias fueled by sticky core PCE.

➤ By intentionally withholding his personal rate projection and launching five technical task forces, the new Fed Chair has effectively introduced a strategic buffer to insulate the Fed from impending mid-term political noise and projecting long-term institutional independence from external influences.

➤ While prolonged “higher-for-longer” baseline through mid-2027 will likely inflate global term premiums and keep US yields elevated, Malaysia’s robust macroeconomic fundamentals and deep institutional liquidity should buffer domestic sovereign curves against severe parallel yield curve shocks.

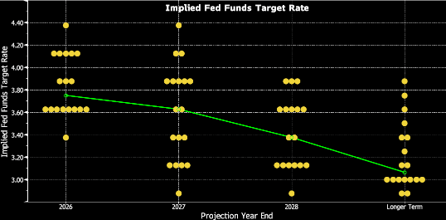

- The Federal Reserve maintained the federal funds target range at 3.50%–3.75% in its first decision under Chairman Kevin Warsh. The current median projection for the federal funds rate at the end of 2026 is 3.8% up from 3.4% in March 2026, indicating at least one rate hike. Following the decision, US Treasury 2-year yield rose by 13 bps to 4.18% while the Dollar Index strengthened by 0.55% to 100.09.

- Chairman Warsh signaled a clear shift in policy communication, moving away from the forward-guidance framework towards a more restrained, data-dependent approach reminiscent of Greenspan era. He also underscored price stability as the Fed’s primary objective and outlined efforts to reduce the central bank’s market footprint in anchoring market expectations.

Chart 1: Fed’s June Dot Plots.

Source: US Bureau of Economic Analysis, RBC Economics.

- As a result, only 18 participants submitted projections in the latest Summary of Economic Projections (SEP) as Chairman Warsh abstained, citing longstanding concerns that the current SEP framework constrains policymaking and is not well-suited to prevailing economic conditions.

- Additionally, the policy debate has shifted from how long the Fed will remain on hold to whether further tightening may be needed. Nine out of 19 policymakers now expect at least one rate hike by end-2026, with six of them believe that more than one quarter point hike will be necessary. Similarly, the CME Fed Watch is also reflecting a 48.9% probability to September rate hike, indicating strong likelihood of monetary policy tightening.

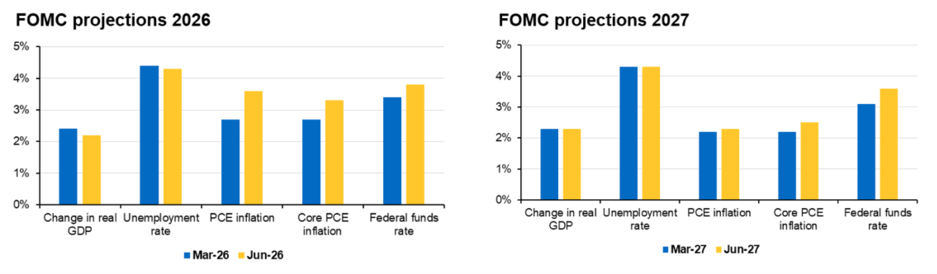

- While recently announced US-Iran ceasefire is expected to reopen the Strait, the timing of a full recovery in oil exports remains uncertain, leaving second-round inflationary effects an ongoing risk. Headline and core PCE inflation (excluding food and energy) forecasts were revised higher to 3.6% and 3.3% respectively in 2026, up from the earlier March FOMC estimate of 2.7%. Both were projected to ease to 2.3% and 2.5% in 2027 implying transient energy-driven price effect alongside sticky price pressures.

Chart 2 & 3: FOMC notable projection changes to 2026 macro outlook.

Source: US Bureau of Economic Analysis, RBC Economics.

- Meanwhile, the 2026 GDP forecast has been revised slightly downward to 2.2%, compared to 2.4% projected in March while the long-term growth remains unchanged at 2.0%. The unemployment rate forecast has also been marginally improved to 4.3%, from 4.4% previously projected in March.

- In his terse policy statement remarks, Warsh announced sweeping internal review of the Fed’s mechanics. He enlisted top economic minds from both inside and outside the Fed to form five independent task forces:

➤ Inflation Targeting Frameworks: Re-examining structural drivers of inflation and moving past failed models.

➤ Productivity and Jobs: Evaluating profound macroeconomic impacts of broad-based technologies, specifically Artificial Intelligence (AI).

➤ Data Quality: Modernizing information sourcing to give policymakers real-time, actionable data rather than lagging indicators.

➤ Fed Balance Sheet: Reviewing the size, composition, and underlying mechanics of the Fed’s balance sheet.

➤ Fed Operations/Communications: Streamlining how the Fed speaks to the public as evident in the newly shortened FOMC statements.

Opus View

- Greater uncertainty is expected under Chairman Warsh’s bold shift toward a “Greenspanera” of monetary policy as visibility over guided rate path moving forward is reduced. This transition is likely to increase market volatility and drive a broader repricing of risk assets. As a result investors may demand a higher term premium, exerting upward pressure on longerdated Treasury yields and supporting continued strength in the US dollar.

- As we observed, Fed Chair Warsh’s first meeting was purposefully intended to project Fed’s institutional independence from external influences by removing himself from the dot plot and launching technical task forces, he has insulated the Fed from November mid-term elections noise.

- As immediate outlook leans towards a hawkish pause, our baseline expectations have pivoted towards an extended higher-for-longer policy rate, with the path toward any monetary easing pushed further out to mid-2027 as transient inflationary pressures diminish, while policymakers remain vigilant to lingering tightening risks. Any policy relief will likely be incremental and entirely contingent on realized supportive macroeconomic data.

- Malaysia bond market has demonstrated idiosyncratic resiliency supported by robust macroeconomic fundamentals and deep institutional liquidityanchoring MGS / GII yields to buffer any meaningful parallel upward shift in the yield curve. However, persistent global inflation and elevated US yields are expected to cap the performance of domestic fixed income market, keeping local government bond yields elevated at current levels and limiting the scope and pace of further yield compression.

Disclaimer

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity. Individual investors should contact their own licensed financial professional advisor to determine the most appropriate investment options. This material contains the opinions of the manager, based on assumptions or market conditions and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information provided herein may include data or opinion that has been obtained from, or is based on, sources believed to be reliable, but is not guaranteed as to the accuracy or completeness of the information. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. Opus Asset Management Sdn Bhd and its employees accept no liability whatsoever with respect to the use of this material or its contents.