16 May 2025

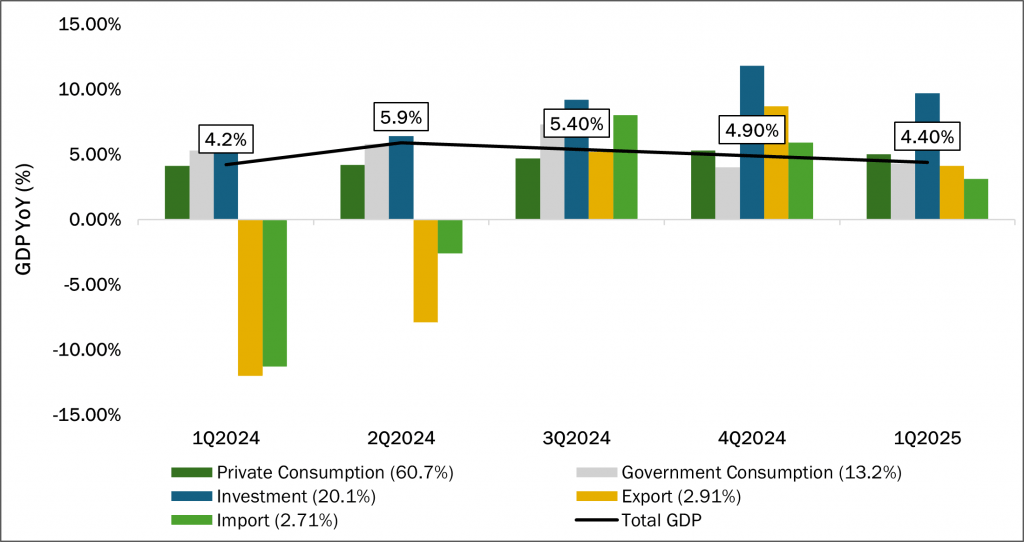

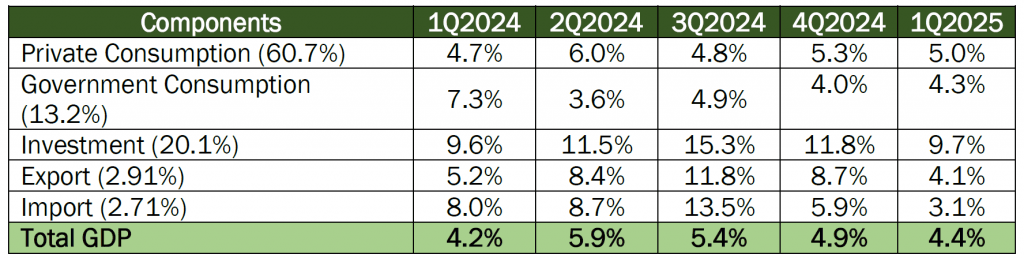

- Malaysia’s Q1 2025 Gross Domestic Product (GDP) grew by 4.4% YoY (Q4 2024: 4.9% YoY), aligning with government forecasts but falling short of market expectations of 4.5%. This marked the third consecutive quarter of slowing growth and the weakest performance in a year, driven by moderating domestic demand and external trade headwinds. Private consumption growth eased to 5.0% YoY (Q4 2024: 5.3%) amid inflationary pressures and reduced subsidies. Government spending rose 4.3% YoY (Q4 2024: 4.0%), supported by infrastructure investments, while fixed investment surged 9.7% YoY (Q4 2024: 11.8%), fuelled by data centre projects and manufacturing expansions. Exports growth decline to 4.1% YoY (Q4 2024: 8.7%), led by electrical and electronics (E&E) products, though weaker global semiconductor demand and U.S. tariff risks dampened trade momentum.

- Sectoral performance revealed diverging trends, with mining contracting sharply (-2.7% YoY) due to lower oil and gas output. Construction growth moderated to 14.2% YoY (Q4 2024: 20.7%) amid input cost inflation, while manufacturing growth marginally declined at 4.1% YoY (Q4 2024: 4.2%), underpinned by E&E and petroleum products. The services sector moderated to 5.0% YoY (Q4 2024: 5.5%), driven by transportation, storage, and business services, though wholesale/retail trade softened. Agriculture rebounded modestly (+0.6% YoY), aided by improved fishing yields, though palm oil production growth slowed. On a quarterly basis, GDP grew 0.7% seasonally adjusted, recovering from a 0.2% contraction in Q4 2024, reflecting resilient domestic activity amid external uncertainties.

- The outlook remains clouded by escalating global trade tensions particluarly US tariffs set to take effect in July unless firm trade negotiations mutually agreed. Bank Negara warned domestic growth in 2025 will likely fall below its official 4.5-5.5% forecast, with balance of risk tilted to the downside. The central bank had lowered the Statutory Reserve Requirement (SRR) from 2.0% to 1.0%, injecting liquidity worth up to RM19 billion, while retaining the Overnight Policy Rate (OPR) at 3.0%. While inflation remain moderate at 1.5% in Q1 2025, the US Dollar weakening and improved investor sentiment post-tariff negotiations offer cautious optimism. Malaysia’s economic resilience hinges on sustained infrastructure spending and robust domestic consumption to mitigate headwinds from weaker global growth.

Opus View:

- Malaysia’s economy remains resilient in 2025, despite growth is moderating amid external headwinds. However, escalating U.S.-China trade tensions and potential tariff spillovers pose risks to export-oriented sectors, particularly semiconductors and E&E. The outlook has become more cautious amid heightened global trade tensions and policy shifts, with the IMF revising Malaysia’s full-year GDP growth forecast to 4.1% from 4.7% previously. We are of the view that the domestic growth is likely projected to be 4.0 – 4.5%, underpinned by slower external growth and supply chain disruption.

- With the latest lower Q1 2025 GDP prints we expect Bank Negara Malaysia (BNM) to potentially lower the OPR rate by at least 25 bps in the 2H2025. Hence,we expect the current yields have priced in the expected cuts with limited upside potential for rates. We aim to tactically lengthen duration to between 5 – 7 years, while focusing on high quality corporate bond to mitigate downgrade risk and for additional yield pick-up.

Disclaimer

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity. Individual investors should contact their own licensed financial professional advisor to determine the most appropriate investment options. This material contains the opinions of the manager, based on assumptions or market conditions and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information provided herein may include data or opinion that has been obtained from, or is based on, sources believed to be reliable, but is not guaranteed as to the accuracy or completeness of the information. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. Opus Asset Management Sdn Bhd and its employees accept no liability whatsoever with respect to the use of this material or its contents.