24 April 2026

SUMMARY

➤ The US–Iran conflict has evolved into a high‑stakes maritime siege, severely disrupting global energy supply. The IEA warns it could take up to two years for markets to return to pre‑conflict conditions.

➤ Malaysia’s fiscal position remains partially insulated by oil and LNG revenues, with each US$10/bbl oil price increase generates ~RM3.5bn in windfall revenue, helping offset subsidy costs. Based on our projections, the 2026 fiscal deficit is expected to range between 3.6% and 3.8% of GDP.

➤ Malaysia’s economic outlook remains resilient, with 2026 GDP growth outlook revised upwards by several institutions despite persistent downside risks. Inflation should remain manageable, anchored by strategic subsidies. We project the OPR to remain at 2.75% throughout 2026 as real rates remain positive.

➤ We remain focused on shortening the duration range to 4.0 – 5.0 years, with an overweight position in high-grade corporate bonds that offer competitive risk-adjusted returns. We continue to prioritise generating meaningful carry‑and‑roll‑down returns by selectively participating in attractive new‑issue opportunities.

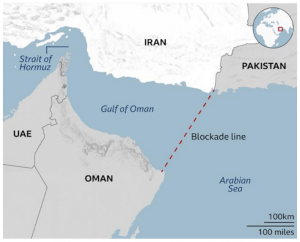

Chart 1: US blockade line in Gulf of Oman

Source: US Department of Defense, BBC.

- The US-Iran conflict has reached a volatile stalemate following the US blockade of Iranian ports on 13 April, after the breakdown of peace talks in Islamabad. As the theatre of war shifted from active bombardment to a high-stakes maritime siege, the global economy faces one of the most significant energy supply disruptions in history. Vessel transits in the Strait collapsed to around 10–11 vessels in early April, compared with a pre-war average of 138 transiting vessels.

- The situation in the Middle East (‘ME’) has further escalated. The US Navy’s 5th Fleet is actively intercepting and diverting all vessels bound for, or departing from, Iranian territory to sever Tehran’s economic lifeline. The fate of a possible second round of peace talks is uncertain, with the ceasefire potentially collapsing after the US military fired on an Iranian-flagged cargo ship heading towards Iran’s Bandar Abbas port.

- The International Energy Agency (IEA) estimated that global energy markets would require up to two years to return to the pre-conflict baseline. Global oil supply plummeted by 10.1 million barrels per day (mb/d) in March, with a further anticipated drop of 2.9 mb/d to 94.2 mb/d in April.

- Production recovery depends on restoring exports. However, trapped tankers, shut-ins, limited storage, and redeployed vessels may delay restarts. Around 390 vessels, including 210 laden tankers, have been choked in the Strait since the conflict started, with only 49 tankers having exited on a net basis

- While half of shut-in oil fields in the Mideast Gulf could return to pre-war output within weeks of export resumption, and up to 80% within a month, the remaining 20% may prove harder to fully restart due to technical issues (e.g., “pressure depletion” or pipeline flow impairment) and interrupted supplies of gas and power.

- According to Rystad Energy, the repair and restoration cost to the region’s energy-linked infrastructure could reach US$58 bil, with total costs for oil and gas facilities expanding to US$50 bil, inclusive of an average US$8 bil across industrial, power, and desalination assets.

NAVIGATING FISCAL TRADE-OFFS AMID MIDDLE EAST CONFLICTS

- Fuel subsidies have traditionally acted as a stabilising buffer against domestic oil price volatility and inflationary pressures, effectively decoupling Malaysia’s CPI from global energy shocks. Without these interventions, the transportation component of the CPI, which accounted for 11.3% of the CPI weight, would have pushed headline inflation towards a 5%–7% YoY range.

- Recent oil supply disruptions and higher prices have led the government to expand subsidy support, albeit in a more targeted and calibrated manner to contain leakages.

- Tighter retail subsidy quotas for BUDI95 from RM300 to RM200 per month;

- Increased cash assistance for BUDI Agri-Komoditi and BUDI Diesel Individu to RM400 per month;

- Higher ploughing incentives for paddy farmers for the 2026 planting season from RM140 per hectare to RM300 per hectare;

- Relaxation of the special permit requirement for diesel purchases exceeding 20 litres for non-vehicle use.

- Federal petrol subsidy expenditures surged to circa RM4 bil per month in March, compared with a pre-conflict baseline of ~RM700 mil. The government has signalled a readiness to increase subsidy allocations of up to RM7 bil in April. Despite the tenfold fiscal allocation, the government remains committed to maintaining a fiscal deficit of 3.5% in 2026, banking on higher petroleum income tax (PITA) revenues from Petronas to offset the subsidy costs.

- Despite being a net fuel importer (consumption: 700k barrels/day; production: 350k barrels/day), Malaysia maintains adequate energy security via 60% crude self-sufficiency and as a net LNG exporter. For every US$1 per barrel increase in global oil prices, it is estimated to generate RM300 mil in additional revenue for the government (excluding upstream dividends to the federal), while fuel subsidy costs are projected to rise by RM450 mil, with a net fiscal gap of RM150 mil.

- By April 2026, every US$10 oil price increase generates RM3.5 bil in windfall, partially offsetting the record RM7 billion monthly subsidy bill. Malaysia is also one of the top global exporters of liquefied natural gas (LNG), with every US$5 per million British thermal units (MMBtu) increase in natural gas prices adding approximately 1.23% of GDP to Malaysia’s current account.

Table 1: Impact of Malaysia’s fiscal deficit based on ME ceasefire solution scenario

| Full year 2026 | ||||||

|---|---|---|---|---|---|---|

| Scenario | Average Brent crude oil price | Additional subsidy | Additional Revenue | Fiscal Expenditure | Fiscal Revenue | Fiscal Deficit |

| Permanent opening of the Strait in 2Q26 | USD85/barrel | RM23.3bil/td> | RM23.9bil | RM442.4bil | RM366.2bil | 3.6% |

| Permanent opening of the Strait in 3Q26 | USD92/barrel | RM32.0bil/td> | RM28.7bil | RM451.2bil | RM371.0bil | 3.8% |

Source: Bloomberg, OpusAM.

- Our in-house analysis expects a marginal shift from the official fiscal target of 3.5%, as rising subsidy costs are likely to be offset by higher oil revenue. Hence, should the Strait be permanently opened with a long-term peace agreement (2Q26 average Brent crude: US$85 per barrel), the deficit is forecast to increase marginally to 3.6%. If the peace resolution is pushed back to 3Q26 with an average Brent crude price of US$92 per barrel, the fiscal gap could widen to 3.8% under the projected 15% increase in additional subsidy outlays.

STABLE INFLATION SUPPORTS STEADY POLICY RATE OUTLOOK FOR MALAYSIA

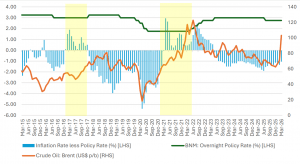

Chart 2: Historical policy tightening cycle and brent crude oil price.

Source: LSEG, OpusAM

- Despite higher energy costs, March CPI held at 1.7%, anchored by strategic subsidies. We forecast 2026 inflation to average 1.6% – 2.0% (2025 Average: 1.4%) within the central bank’s tolerance range. While the subsidy cushions the impact of global oil volatility, any subsidy rationalization may shift inflation trajectory towards the upper bound of the official threshold range that could potentially pivot BNM’s policy rate decisions towards maintaining positive real rate of returns.

- Historically, monetary policy has tended to tighten in periods in which inflation exceeded the policy rate for a sustained duration of around 12 months. This is consistent with empirical evidence that second-round inflationary effects typically materialize with a 6 – 12 month lag in Malaysia

- With positive real rates of return and a current gap of 1.05% between inflation and the policy rate, the buffer provides BNM with sufficient policy headroom to maintain current OPR levels to support domestic economic and credit growth. As such, the policy rate is likely to stay on hold at 2.75% at least until inflationary spillovers broaden across non-energy sectors

DOMESTIC RESILIENCE & SAFE-HAVEN FLOWS SUPPORT MALAYSIA’S OUTLOOK

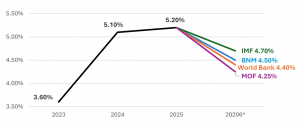

- In its latest published Economic and Monetary Review, BNM (BNM) projects Malaysia’s economy to expand by 4% to 5% in 2026 surpassing earlier projection of 4% to 4.5%. This growth is expected to be firmly anchored by resilient private sector consumption, low unemployment rate of 2.9% and steady wage growth. Headline inflation is projected to average 1.5% to 2.6% (previously: 1.5% – 2.3%), reflecting heightened external cost pressures, particularly from energy‑related inputs

Chart 3: Malaysia’s GDP growth (%).

Source: IMF, BNM, World Bank, MOF, OpusAM

- Given that Malaysia has entered the crisis from a position of strength following solid 1Q2026 advanced GDP growth of 5.3% YoY, the World Bank raised Malaysia growth forecast to 4.4% for 2026, citing resilient private consumption underpinned by wage gains and favourable labour market dynamics. Similarly, the IMF also lifted the GDP growth projection to 4.7% in April 2026, highlighting the country’s diversified export base and strong domestic demand.

- Nevertheless, downside risks to growth remained elevated as external risks weighed on Malaysia’s growth prospect amid trade tariffs uncertainty, elevated global energy prices, and prolonged geopolitical conflicts. Persistent disruption to the global supply chains, dampen investment sentiment, and moderating the pace of private capital expenditures expansion.

- In the current climate of heightened geopolitical instability, Malaysia has increasingly emerged as a regional safe harbor for international capital. Foreign fund flows into the domestic bond market rebounded significantly, reaching a net inflow of RM6.1 bn in March 2026 following a net outflow of RM2.5 bn February. This strong momentum was primarily driven by a fund reallocation away from other Asian markets that are highly vulnerable to oil supply disruptions.

BOND MARKET OUTLOOK AND OPUS VIEW

- Malaysia’s bond market remained resilient despite external headwinds, underpinned by wellanchored inflation, strong macroeconomic fundamentals, and prudent monetary policy. The ME conflict triggered geopolitical repricing across the yield curve, particularly in the short-tointermediate segment, which climbed by circa 4 – 16 bps, while the 10-year MGS benchmark yield rose to 3.56% on 23 April from 3.49% at the start of the conflict.

- The AAA-rated corporate bond and sukuk yields rose in 1Q26, reflecting global risk aversion and inflation repricing rather than domestic credit deterioration. Spreads widened by 5 – 10 bps across credit quality as domestic heavy issuances weigh on spreads amid heightened geopolitical risk premia and rising inflation expectations.

- The issuance pipeline is projected to remain healthy, driven largely by increased refinancing requirements, as larger volumes of government and corporate bonds are set to mature in 2026. Stable OPR expectations at 2.75%, ample domestic liquidity, and tight credit spreads have incentivized issuers to front-load their issuances in lieu of upside risks to global yields.

- Under current environment of anchored yields and persistent uncertainty, we continue to focus on quality and duration defensive positioning. We have been actively reducing our portfolio duration since November 2025 from 4.0 – 6.5 years to 4.0 – 5.0 years while maintaining our overweight in high-grade corporate bonds with strong fundamentals to optimize risk-adjusted returns while preserving capital.

- Additionally, the heavy issuance pipeline and the steepening of benchmark yield levels have improved valuation appeal, creating attractive entry opportunities in new-issue premiums that offer favourable coupon carry. With yields sufficiently elevated and steepest in the intermediate segment (3 – 10 years), we are also able to generate meaningful carry-and-rolldown strategies without requiring excessive long-duration positioning.

Disclaimer

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity. Individual investors should contact their own licensed financial professional advisor to determine the most appropriate investment options. This material contains the opinions of the manager, based on assumptions or market conditions and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information provided herein may include data or opinion that has been obtained from, or is based on, sources believed to be reliable, but is not guaranteed as to the accuracy or completeness of the information. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. Opus Asset Management Sdn Bhd and its employees accept no liability whatsoever with respect to the use of this material or its contents.